Duet Protocol Global Market Recap and Outlook — 20231127

Unlock the full potential of your trading strategy on pro.duet.finance! 🚀

Experience up to 100x leverage, dive into 30+ assets including FX, stocks, commodities, indices, and more, all in a highly liquid & smooth platform. Plus, enjoy the industry’s highest reward ratio with up to 80% trading fees returned to you! Hedge against crypto dumps and access traditional markets without leaving the crypto sphere. 💸📈💹

#TradeWithDuet #CryptoMeetsTraditional

In shortened holiday trading, US stocks edged up, bonds fell slightly, the dollar dropped, crypto and gold rose, oil was flat, with overall market sentiment optimistic. The S&P 500 is now near July highs while the Nasdaq is slightly above July peaks. This rebound has mainly been driven by falling secondary market rates, institutional passive repositioning, and the corporate buyback window, against a backdrop of strengthened conviction in peak rates rather thanimproving economic or earnings fundamentals. Fund flow changes could spur wider oscillations.

Crypto hovering near highs with both BTC and ETH oscillating around April 2022 tops while altcoins lag:

Implied volatility has fallen back to historical lows, often a reversal signal:

Hedging demand has plunged sharply, cutting the cost of insuring against market dumps by around 10% (1 standard deviation), dropping to the lowest level in the data since 2013. Demand to hedge tail risks also hovers around March lows.

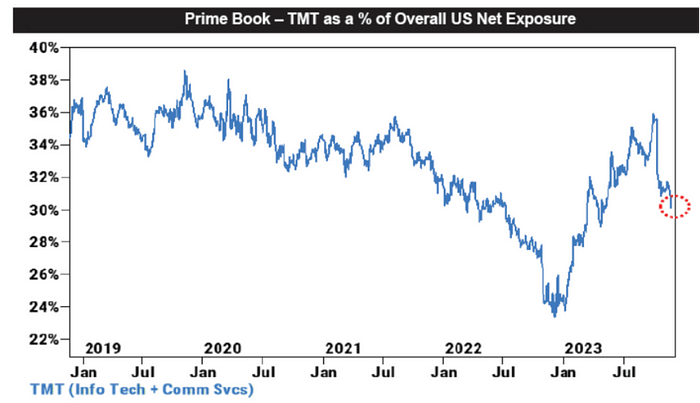

Despite the broad market rise in recent weeks, tech stock dumping has been a noticeable undercurrent. According to GS Prime Book data, US tech saw largest net selling since July last week, mainly longs built up earlier now reducing exposure. Long unwind volumes exceeded short covers.

Tech share of GS Prime client net exposure dropped to 30%, from around 36% in late October. Overall the 30% share is at 36th percentile of past year, 16th percentile over 5 years, not stretched.

This week is another major issuance week with Treasury selling $54 billion 2Y and $55 billion 5Y Tuesday Nov 27, then $39 billion 7Y Wednesday Nov 28th. Auctions have been an important volatility catalyst for markets overall. Last week’s poor demand for $15B 10Y TIPS and $26B 2Y on Wednesday drove yields initially lower before the strong $16B 20Y auction Monday brought a sharp reversal higher in yields, especially the front-end:

Bond markets could also face turmoil from Europe. A German court ruling to subtract €60 billion of spending from the federal budget reduces usable funds by €60 billion. Germany will again suspend its debt ceiling, potentially spurring bund issuance. Dropping the expenditures could subtract 0.5 percentage points from German GDP. Neither is good news but still early days for this case. The court ruled using €60 billion of pandemic relief money for climate protection from 2021 onward was illegal, raising speculation on whether the €770 billion of cumulative off-budget special funds might also face illegality rulings.

Separately last week saw UK and Canada report fiscal deficits over expectations as well, adding up to increased sovereign debt supply globally being an unavoidable mega-trend, question is when it becomes a speculation theme again.

Both Powell and the Fed minutes mentioned sustained tightening financial conditions could substitute for hikes. However conditions have not tightened persistently, with policy now 50% reversed from October:

But with employment also one of the Fed’s two core objectives, further labor market softening could still prompt easing even with inflation above target.

Bond yields dropping from 5% to 4% imply soft landing, should be bullish, but dropping from 4% to 3% would reflect recession concerns, risk asset downside. So best case is yields hover around current levels without falling much more.

On currencies, the USD extended declines last week but the drop narrowed. USD weakness benefits commodity assets. Over the past two weeks, the yuan rallied 2% vs the USD to 7.14–7.15 but gains did not lead major currencies:

Nvidia Earnings Smash Estimates

Q3 revenue doubled YoY while EPS profit nearly sextupled, far exceeding Street forecasts:

Q3 revenue $18.12 billion, up 206% YoY versus 171% Street forecast at $16.09 billion, nearly 13% higher and well above Nvidia’s own $15.68–16.32 billion guidance range. Q2 revenue rose 101% YoY.

Q3 non-GAAP EPS $4.02, up 593% YoY against 479% expected at $3.36, nearly 20% higher. Q2 EPS rose 429%.

Q3 non-GAAP gross margin 75.0%, up 18.9 percentage points YoY, above 72.5% forecast and 72–73% guidance range. Up 3.8 percentage points sequentially.

But the strong report failed to lift shares like usual, with NV stock down 3.5% last week, showing prevalent investor wariness at current levels after the 240% YTD gain, taking profits amid any hints of slowing growth persistence that the Street hopes continues for years. Some cite concern on US export controls to China limiting GPU sales though Nvidia believes robust overall demand can fill that gap. Overall market action shows skepticism on that view. Shares extended declines the next day after Nvidia delayed launch of a new China-customized AI chip meeting latest US export rules.

For tech stocks, Nvidia has been a reliable leading indicator for most of this year so the contrarian weakness is not an encouraging signal.

Valuation-wise, NV trades at a 30x P/E on the $16.6 CY 25 EPS forecast which isn’t stretched. AMD for instance is around 32x. Nvidia’s long-term challenges are mainly twofold — many clients including Microsoft and Intel are developing their own AI chips to reduce reliance, and any bursting of the AI bubble could eliminate data center chip demand.

OPEC+ Meeting Postponed

With disagreements on production cuts, the delayed OPEC+ meeting initially scheduled this coming week has drawn market attention as calendar changes are rare major events at that level. The core contradiction is Saudi Arabia, Russia, and other cut advocates wanting deeper reductions from other members. The surprise delay led to greater oil price volatility last week with a 10%+ drop in the past six weeks. The rescheduled meeting holds great significance since oil prices are key to next year’s rates and markets. Separately, ahead in polls, former President Trump commented that if elected, he would scrap Biden’s climate law and “maximize fossil fuel production” pointing to additional volatility drivers from geopolitics.

Argentina “Fully Dollarizes” Economy

Far-right electoral coalition “Freedom Advance” candidate Milei won Argentina’s presidential election. Milei advocates fully dollarizing, closing the central bank, slashing welfare, and other radical measures. Argentina currently has one of the highest inflation rates globally around 140%. Milei hopes dollarization can boost confidence and contain currency devaluation. Many see him as Argentina’s savior. After his victory, Musk also capitalized on the moment, commenting “Argentina prosperity is coming.” However with negative net FX reserves, it is unrealistic for the central bank to acquire enough dollars to exchange in the near term, leaving extreme peso devaluation still a huge risk. Separately, Milei “sees Bitcoin as a key tool to counter the inefficiencies and corruption of the centralized financial system” and a “viable alternative to traditional economic structures”, so his election is seen by crypto players as the beginning of broader integration of cryptocurrencies to address Argentina’s problems with inflation and financial instability.

However, Milei’s post-election speech lacked the flamboyance promised on the campaign trail, warranting some reduction in expectations priced in on his radical policies.

Looking at results from El Salvador which pioneered adopting crypto as legal tender, actual adoption remains scarce domestically (remittances received in Bitcoin were only around 1% in the first 6 months of 2023 according to the central bank, as transaction speeds and costs of Bitcoin are not conducive for daily payments but offer huge advantages for cross-border transfers, with the World Bank estimating average fees of 6% on $200 international money transfers). But it contributed to a bounce in El Salvador bonds (0.26–0.8). Bitcoin’s strong performance this year was a key background factor, somewhat similar to MicroStrategy. In summary Bitcoin has not shown a tendency to become actual currency but acted as a reserve asset outperforming the dollar.

With no public government record, the exact BTC amount held by El Salvador remains unclear. Following prior schedules, holdings are estimated to have reached 2,744 bitcoins as of Nov 14 (worth $100 million now) with average purchased price around $41,800 — still showing several million in losses at current prices.

Israel-Hamas Truce

The temporary Israel-Hamas truce took effect last Friday, requiring cessation of hostilities for at least four days with prisoner exchanges and increased Gaza humanitarian aid during the period. As only brief relief, impact was limited on financial markets. Gold closed back above $2000 last week.

Robust Thanksgiving Spending

Consumers have shown surprising resilience this year, powering through inflation, spiking rates, and resumed student loan repayments. According to Adobe, US consumers spent a record $5.6 billion online on Thanksgiving Day itself, up 5.5% YoY, while Black Friday hit $9.6 billion, up 6%. The National Retail Federation expects over 182 million people will shop over the Black Friday promotional period, a 9% YoY increase to set the highest level since tracking began in 2017. Per Deloitte, average consumer spend during the long weekend should rise 13% YoY to $567. NRF estimates Thanksgiving to New Years consumer spending from $956.3–966.6 billion, at least 3% higher than 2021 but likely just keeping pace with inflation, confirming recent trends of lower promotional discounts offsetting still-rising underlying demand.

UBS: Fed Rate Cuts Plus Plunging Real Yields Taking Gold To New Highs in 2023

Precious metals analyst team led by UBS’ Joni Teves stated in their latest annual gold outlook that investors are currently not highly positioned in gold, unwinding most exposure over the multi-year recovery from the pandemic. But positioning will shift as the cycle matures and policy pivots.

UBS expects Fed rate cuts starting in Q1 2024. A December pause would reinforce tendency to cut around 6 months after final hike.

Examining post-hike-cycle gold performance, UBS found prices typically drop 2% around 3 months after previous tightening ends then rally 7% over the following 6 months.

UBS believes recession-driven Fed cuts, weaker dollar from easing, and 160 basis point plunge in 10Y real yields from 2023 highs could take gold to new record highs in 2024–2025.

Under UBS’ baseline forecast, gold reaches $2,000/oz by year-end, then $2,200 in 2024 and $2,100 in 2025 while holding near peak levels.

(Much of gold bull case logic is applicable to Bitcoin as well when it comes to the alternative allocation’s preparation for lower eventual rates)

JPM AM: Alternatives Allocation Crucial in 2023

With stocks and bonds likely staying highly correlated as inflation pressures ease alongside slowing growth, higher correlations increase diversification value from alternative investments. Alternatives also offer yield premiums now while poised for solid expected returns.

(This logic also applies in crypto markets. Regardless of whether you believe in it, Bitcoin’s historical price Sharpe/Sortino ratios exceed even the Nasdaq 100, making it hard to ignore within alternative asset allocation selection setting it apart from most alts)

Chinese Property Stocks and Bonds Rally

China is apparently pressuring banks to support embattled property developers, allowing lenders to offer unsecured short-term loans to qualified firms. Sources said authorities are finalizing a draft list of 50 eligible developers. Last week Chinese developer equities and bonds rallied on the news. For instance, Country Garden soared 20%, Longfor 50%, CIFI 50%, while the MSCI China Real Estate ETF rose 10% and Shanghai property index 2–3%. Most Chinese developers face liquidity not solvency crises, meaning sufficient cash injections let them survive. Ignoring problems would exacerbate stalled projects and vicious cycles. With up to RMB 3 trillion likely needed, market absorption is unrealistic making debt monetization the only solution.

Positioning and Fund Flows

Overall equity exposure pushed further into moderately overweight territory this week at 58th percentile, particularly discretionary positioning surging to highest since late-July at 78th percentile but not extreme highs yet. Systematic edged up slightly but remains below neutral at 38th percentile:

Equity funds logged a third straight week of inflows ($13.1 billion) with the US ($12.4 billion) taking the bulk again. Bond fund inflows ($6.7 billion) accelerated with investment grade ($4.1 billion) seeing largest weekly haul since early April. Money market funds extended inflows to a 5th week ($30.9 billion), totaling over $222 billion in the stretch.

Recent flows were clearly into telecom and tech, also financials, while utilities, healthcare, energy saw notable outflows:

Since October, performance for highest shorts (top 10%) has caught up:

CTAs sharply raised equities allocation back to neutral territory at 25th percentile:

According to BoA’s analysis, CTAs will likely stay aggressive equity buyers this week:

On BTC futures, asset managers (blue) continue extending record net longs while retail (purple+red) turned net short last week. Market makers (grey) notched 52-week high shorts. Leveraged funds (green) also reduced but maintain elevation. We previously analyzed the bulk of asset manager rise as from BTC futures ETFs so most other players are not actively positioning long despite ETF inflows reaching over $1 billion now. Historically the leveraged funds’ tendency to cut longs into strength and rebuild on weakness is very noticeable. While other futures participants are clearly still short, this could partly signal peaks to them but if wrong, the short cover momentum would be necessarily powerful.

Sentiment

BofA Bull & Bear indicator rose to 2.1, shifting sentiment from extremely bearish to neutral. They advise cautious optimism at this level:

CNN Fear & Greed index surged into Greed zone:

AAII and Goldman updates not available this week.

Unlock the full potential of your trading strategy on pro.duet.finance! 🚀

Experience up to 100x leverage, dive into 30+ assets including FX, stocks, commodities, indices, and more, all in a highly liquid & smooth platform. Plus, enjoy the industry’s highest reward ratio with up to 80% trading fees returned to you! Hedge against crypto dumps and access traditional markets without leaving the crypto sphere. 💸📈💹

#TradeWithDuet #CryptoMeetsTraditional

Join us:

Github| Medium| Telegram| Twitter | Website |Discord | YouTube