Duet Protocol Global Market Recap and Outlook — 20231009

Market Overview

Over the past two weeks, major global stock markets fell, with only the NASDAQ recording a biweekly increase.

The US dollar remains strong, with the Japanese Yen showing signs of weakness and the offshore RMB remaining stable.

Cryptocurrencies strengthened, while energy and metals softened. Notably, Saudi Arabia expressed willingness to increase oil production to facilitate a “US-Saudi Mutual Defense Agreement,” leading to a 7% drop in oil prices. However, recent conflicts between Israel and Palestine might drive oil prices up again.

Long-term US Treasury yields strengthened significantly.

There was no significant change in the strength and weakness of cyclical and defensive sectors.

Large-cap stocks continue to outperform small-cap stocks.

The most important event of the past week was the US government’s release of the September jobs report on Friday, which showed job growth far exceeding everyone’s expectations. The market’s first reaction was panic, with the 10-year Treasury bond price plunging nearly 2% and stocks seeming set for further declines, while CME’s FedWatch tool showed the probability of a November rate hike jumping 10 percentage points to 82%. But that eventually settled back to 27%, unchanged.

However, the situation quickly reversed, with the S&P 500 index bottoming and closing up 1.2% within the first half hour of trading. The 10-year Treasury bottomed around 10:50 am, recovering about a third of its losses. The odds of a rate hike also edged back from earlier highs.

The 10-year US Treasury yield climbed to its highest level since 2007 of 4.88% on Friday. It closed around 4.8% on Friday, well above 3.3% six months ago. The 30-year US Treasury yield briefly topped 5% Friday morning before falling back below the threshold to close at 4.97%.

With long-term yields rising faster recently, the yield curve inversion has improved notably, with the 10–2Y now only inverted by 30bp. But there’s still a long way to go to restore a normal upward sloping curve. If the 2Y holds around current 5.08%, the 10Y may need to rise over 6% to be considered normalized.

This is because after a brief panic, the market focused more on wage growth hitting the smallest increase since June 2021, nearing the Fed’s 2% inflation target in a significant sign of labor market loosening. It at least means the labor market doesn’t require further aggressive Fed hikes.

September NFP summary: Key sectors of economy continue recovering jobs but wage growth moderated. We believe this gives Fed space to keep tightening policy without severely harming growth (more room but not necessarily will). Market impact is overall neutral with job gains offset by slower wages.

September NFP substantially beat at +336K, the largest monthly increase this year, and prior two months revised up by 119K combined. This shows labor market remains robust.

Job growth continues concentrated in high-contact services like education, healthcare, leisure/hospitality. These added 170K jobs in Sept, 55% of total.

Meanwhile, wage growth was softer with average hourly earnings slowing to 4.2% YoY vs expected. Past 3 months averaged just 3.4% wage growth. Various surveys also show cooling employer willingness to raise wages, suggesting improving balance of supply/demand, favorable for Fed and inflation.

Combination of tight labor market but slowing wages provides basis for Nov Fed hike. Overall report shows labor market still strong but easing inflation pressures.

With both bulls and bears able to cite the report, market reaction was mixed with US yields spiking to new highs but stocks closing up. They often move in opposite direction. Hard for report to be catalyst for stock rebound, Friday’s bounce was more technical. Bear market not over until recession/credit event causes policy shift. Stocks rangebound until then with limited sustained rallies.

In low rate environment, investors focused more on valuations than earnings growth. But now with higher rates, growth will be scrutinized more. Rising rates raise corporate borrowing costs, potentially constraining growth. Whether future rate/inflation impacts offset or not will determine if stocks rebound. Best case is cooling inflation reduces hit to profit margins, unlike earlier when input/labor costs squeezed margins significantly. While easing cost pressures and still-strong growth help margins, hefty wage gains, higher rates/taxes make big profit growth unlikely.

Other Economic Events to Watch

Most Fed officials still see need for high rates for some time, with hawkish Bullard and Mester not ruling out more tightening in November.

August US PCE inflation rebounded to 3.5% YoY, core PCE as expected moderated to 3.9% YoY.

September US Markit Manufacturing PMI final raised to 49.8; Services PMI final revised down.

August US Durable Goods orders growth finalized at 0.1% MoM.

Latest initial jobless claims rose back to 207K.

As of Oct 7, Atlanta Fed GDPNow model estimates Q3 US GDP growth at 4.9% SAAR, unchanged from Sept 29 estimate.

BOJ Sept minutes showed hawkish views, with one hawk saying inflation target achievement was in sight and normalization may not be far off.

US Q3 Earnings Season Arriving

Third quarter 2023 earnings season kicks off this week

The earnings season kicks off this week, with first reporters including Pepsi, JPM, Citi, Wells Fargo, and Blackrock. Early reports are heavy on financials. The season will wrap up quickly, with 80% of S&P 500 companies having reported by Nov 3.

Market expects 0% YoY profit growth for S&P 500 in Q3, most optimistic view entering a reporting period since Q4 2022. Ex-energy expected up 5%, best since Q1 2022. Median EPS growth forecast 2% for individual companies:

By sector, consensus most optimistic on Communication Services EPS (+28%) and most pessimistic on Energy EPS (-38%). Though Brent crude rose 27% in Q3, average price still 12% below year-ago level. Ex-energy, S&P 500 EPS seen up 5%.

Per GS estimates, Information Technology is largest contributor to S&P 500 EPS estimates in both 2024 and 2025, adding 2 percentage points of growth each year. After weak 2022, Communication Services and Consumer Discretionary profits have troughed and are set to jointly contribute ~3 percentage points in 2024 and 2025 from cost initiatives and margin focus at META and Amazon. But corporate investments into AI could limit profit growth in these sectors.

Concentration risk in mega cap techs contributing heavily to S&P 500 sales and profits poses downside risk if companies fall short of expectations. In 2022, Big 7 stocks (AAPL, AMZN, GOOGL, META, MSFT, NVDA, TSLA) accounted for 12% of S&P 500 sales and 17% of profits. By 2025, market expects big tech to contribute 15% of S&P 500 sales and 24% of profits. Antitrust scrutiny by regulators is a potential headwind to future growth for this group, with recently announced lawsuits targeting practices at Apple, Amazon and Google. Our past case studies showed sales growth slowed at AT&T, Microsoft and IBM following settlements of their antitrust cases.

With profits expected to notch a cyclical high this quarter and history of earnings season being net positive for stocks, outlook for next quarter not overly gloomy amid relief from overheated bullish positioning and expectations for strong earnings. Key is whether volatility in Treasuries can be tamed, ie yields shifting from one-way upside to rangebound.

According to bond king Bill Gross, normally such a massive spike in real yields would compress the forward P/E of the S&P 500 from 18X currently to 12X. But excitement over AI potential and massive government spending blunted the impact. Still, “can AI and $2 trillion future fiscal deficits prove ‘this time is different?’” he wrote. “I doubt it.”

Impact of War

The Islamist radical group Hamas launched a sudden attack this weekend, killing over 600 Israelis so far. Saturday was the deadliest day for Israel in decades, as violence between Palestinians and Israelis has surged over the past few months. This long-running conflict now appears to be entering uncharted and dangerous new territory. Israel formally declared war on Hamas on Sunday and carried out airstrikes on the densely populated Gaza Strip in response. Israeli Prime Minister Netanyahu has vowed revenge, warning Israel will take “forceful retaliation” and is prepared for a “long and difficult war.” The Palestinian Health Ministry said at least 413 Palestinians have been killed in Gaza since Saturday.

Additionally, Hamas attacks in Israeli-occupied territory have left several foreigners dead, including Americans and French. Major developed nations have expressed support for Israel, and the US has moved the USS Eisenhower aircraft carrier group closer to Israel.

With financial markets closed over the weekend, the war news did not directly impact markets yet. Crypto markets continued their weak, range-bound price action. Looking back at the last major war, Russia’s full invasion of Ukraine in February 2022, the S&P 500, gold, and crypto all rallied that month, but then declined for the next three consecutive months. However, the Fed was also in a rate hiking cycle then.

Positioning and Fund Flows

Several stock market investor positioning indicators fell again this week, showing bearish sentiment strengthening further.

Systematic portfolio positioning dropped significantly to a neutral 40th historical percentile (deep blue line below). Subjective investor positioning (already in underweight zone) also fell further back to May levels at 29th historical percentile (green line below).

Deutsche Bank analysis shows the earnings season rally magnitude is negatively correlated to positioning at the start of earnings — lighter positioning means a larger rally.

The earnings season rally is also negatively correlated to pre-earnings performance — weaker prior performance means a larger rally.

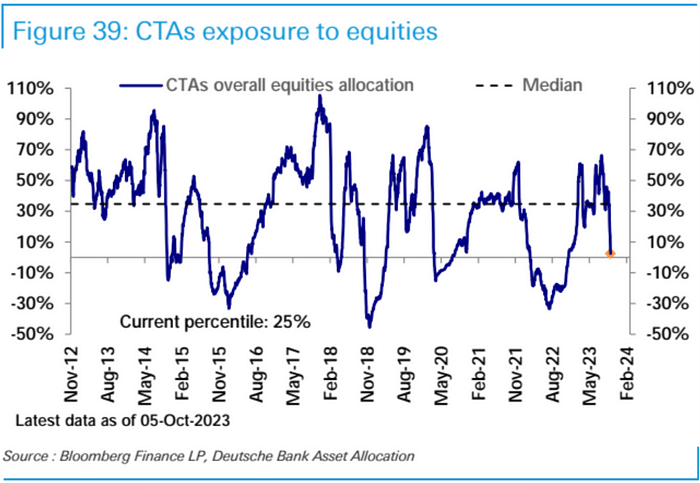

CTA (momentum strategy) overall equity positioning dropped sharply last week, now at 25th historical percentile, signaling light positioning.

At the same time, CTAs are clearly short bonds, extremely long USD, extremely short gold, and extremely long crude oil — a clear structural view. This is getting closer to reversing.

Bullish-bearish S&P 500 options volume continues falling sharply to 9-month lows and sits at a historically unusual negative level (1st percentile).

Equity ETF/mutual fund flows saw a second week of net inflows ($33B) but slower than prior week. US ($39B) and Asia ($12B) inflows slowed while EM saw minor net inflows ($2B). Europe outflows extended to 30 straight weeks ($18B). Bond funds saw net redemptions ($25B) for a second week, driven by corporate and EM bond outflows while govt bonds maintained inflows.

Money market funds saw strongest net inflows ($708B) in three months, reversing prior two weeks of outflows.

Latest CFTC data shows overall US stock futures positioning dropped again, with S&P 500 net longs decreasing and Russell 2000 net shorts increasing. Nasdaq 100 net longs were flat. Dow net shorts by asset managers and leverage funds now exceed 20% of total open interest value:

Alongside the USD bounce, USD net shorts have fallen for three straight months and are nearly back to flat:

Sentiment Indicators

Goldman Sachs Sentiment Indicator is currently at 0.5, in the neutral to positive range:

Bank of America Fund Manager Survey sentiment indicator dropped sharply, now in pessimistic zone

AAII investor sentiment bearish percentage rose to 41.58%, highest since early May, though bullish percentage also had a minor rebound. Neutrals fell sharply, suggesting the bull-bear tug of war may become more pronounced again:

CNN Fear & Greed Index plunged to 17.58 last week, most fearful since October 2021, but rebounded the last 3 days:

Perspective Sharing

[BofA View: Focus on Structural Trades]

With ongoing deleveraging from rising funding costs, recession has high probability of occurring, which is when the market will bottom and rebound. For now focus should be on relative value between assets and sectors, not absolute value.

BofA on Oct 5 highlighted several clear mismatches:

Tech stocks vs US Treasuries

Japan representing “soft landing” vs China “hard landing”

Banks “hard landing” vs Brokers “soft landing”

Transports “soft landing” vs Retail “hard landing”, with former starting to catch down to latter

Small caps flashing US recession signal, so once recession confirmed should pivot from selling “soft landing” to buying “hard landing” concepts

During this waiting for recession, focusing on these mismatch trades is more important than absolute valuation of individual stocks or sectors.

[Dalio Says US Faces Debt Crisis]

Hedge fund founder Ray Dalio said in a CNBC interview, “this country is going to be facing a debt crisis.” He and Marc Lasry spoke at the Managed Funds Association fireside chat. “I think the speed of it is going to depend on the supply-demand situation, so I’m watching that closely.”

Dalio is concerned economic headwinds go beyond just high debt levels, saying growth could go to zero with fluctuations of 1% or 2%.

“I think there’s going to be a significant slowing down of the economy,” Dalio said.

[Who is Driving the Bond Market?]

With supply increase and shifting demand dynamics, US yields may remain elevated. Issuance is up (added $10T last 3 months) while Fed no longer buys, bank demand is down, and institutional risk appetite for bonds is lower. This means Treasuries need higher yields to attract buyers, so hard for 10Y to decline much.

[Evidence for Optimists]

Optimists say cooling inflation will eventually help cap secondary market yields. In early 1980s, inflation peaked and broke below 10Y yields, which also peaked and fell, but with ~1 year lag.

[Robust Consumer Enthusiasm]

US high frequency consumption data rebounded sharply the past two weeks, up 1.8% YoY, or 2.0% ex-gasoline. Stripping out gasoline spending shows consumption growth more clearly. This may mean consumers are spending more on other goods/services despite rising energy costs.

[Cost of Exuberance]

Light blue line shows bank lending standards to corporates have loosened substantially since 2022. Past loosening into euphoric periods preceded spikes in HY default rates, which are now accelerating higher in dark blue:

The End.

Join us:

Github| Medium| Telegram| Twitter | Website |Discord | YouTube