Duet Protocol Global Market Recap and Outlook — 20230828

The risk asset market stabilized in the past week, but the level of entanglement increased. Contradictory trends emerged in the cross-asset market. This is evident as investors now lack further optimistic reasons after the rise of the artificial intelligence theme, better-than-expected US stock earnings, and speculation that the Federal Reserve will turn to rate cuts once the economy cools down. Investor sentiment has recently declined, but this is a positive signal. Moreover, the pessimistic expectations for the Chinese economy seemed to have bottomed out in July. NVDA’s financial report greatly exceeded expectations, but funds chose to exit. As for which long-term beneficiary company stocks to buy after the short-term rise in AI, Goldman Sachs conducted a quantitative analysis.

US Market

Last week, the long-term interest rate rise in the interest rate market took a break, with short-term rates catching up, especially after Powell’s hawkish speech on Friday. The yield on the 2-year bond reached its highest level since March.

Major US stock indices rose last week, with a wide range of fluctuations during Powell’s speech, but eventually closed higher.

The yield gap between stocks and bonds has reached an extreme level of several decades, reflecting increasing caution among investors:

● The current dividend rate of the S&P 500 is about 1.58%, while the 10-year bond rate is about 4.25%. The gap between the two is 2.66%, the largest since 2007.

● The current profit rate of the S&P500 is only 40 basis points away from the 10-year bond rate, the smallest gap since 2004.

During Powell’s speech, the US dollar index recorded an intraday low of 103.75. After his speech ended, it rebounded to a new high since June 1st, reaching 104.45. However, the RMB stabilized last week, closing at 7.288 on Friday, without falling below the important level of 7.3.

Crude oil closed slightly lower, gold, silver, and copper all rose, and cryptocurrencies fell slightly. Gold recorded its best weekly performance since mid-July. Before Powell’s speech at Jackson Hole, the yield on US long-term bonds fell back, providing support for gold prices.

Federal Reserve Chairman Powell’s speech at the 2023 Jackson Hole conference had three main points, but there was no new information: First, the Federal Reserve remains committed to achieving a 2% inflation target, rejecting speculation about tolerating or raising the target. Second, officials are ready to raise interest rates further if necessary and will maintain high borrowing costs until inflation convincingly approaches the target. This means interest rates may remain higher for longer. Lastly, after significant rate hikes since 2022, the Federal Reserve is now cautiously assessing the risk of excessive tightening and will be cautious about future rate hikes, which are not necessarily affected by sustained economic resilience. Additionally, there was no clear guidance on the recent market’s focus on the “neutral interest rate,” so this speech had little effect on resolving the current market uncertainty.

Investors in the interest rate futures market are divided on whether the Federal Reserve will raise interest rates once more this year or maintain the status quo, with odds of another rate hike by the end of the year at about 46% on Thursday. After Powell’s speech on Friday, the odds increased slightly to 53%. By June of next year, traders expect a 62% chance the Federal Reserve will cut rates from the current level, down from their 83% prediction a week ago.

Combined with the stock market rise, the sharp decline in short-term bonds/stability in long bonds/a slight rise in junk bonds, and the market performance of gold and cryptocurrencies fluctuating and eventually levelling out, it is evident that investors currently have divergent views and are evenly matched between bullish and bearish stances.

In terms of market commentary, “Bond King” Bill Gross commented on Powell’s speech on Friday, suggesting that the 10-year U.S. Treasury yield could rise to 4.5% in the future, with short-term rates remaining relatively stable. He interpreted Powell’s subtext as “higher longer”. Former US Treasury Secretary Summers believes Powell’s speech indicates that the Federal Reserve may need to raise interest rates at least once more, if not more. Summers believes Powell’s remarks suggest that the Federal Reserve is open to the possibility that the neutral interest rate may be higher than in the past.

The U.S. economic surprise index fell slightly last week but overall remains at its highest point since April of last year.

US durable goods orders for July fell 5.2% month-on-month, the biggest drop since the outbreak, mainly due to a nearly 44% drop in non-defense aircraft orders after a surge in the previous month.

The US Markit Manufacturing PMI for August was 47, a new low since February of this year. The service PMI was 51, a two-month low. The composite PMI was 50.4, a new low since February. Analysts said weak consumer demand in August nearly stalled business activity, raising doubts about the strength of U.S. economic growth in the third quarter.

Outside the US

The pan-European Stoxx 600 index closed flat. Chinese stock indices mostly declined, but the real estate sector rose on supportive policies like first-home mortgage loans without credit record requirements and tax refunds for improved housing sales. Additionally, Chinese stocks welcomed a combination of supportive policies over the past weekend, including halving the stamp duty tax, optimizing IPO and refinancing regulations, further regulating share sale behavior, and lowering margin financing requirements. Many analysts expect a significant rebound in A-shares this week. Separately, the Hong Kong market also saw news of potentially canceling the stamp duty tax.

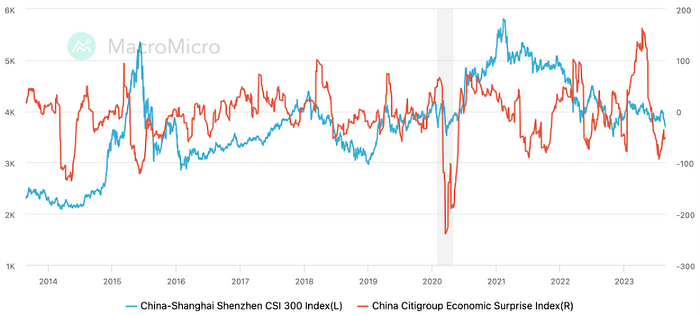

The level of pessimism towards the Chinese economy seems to have bottomed in July. Aside from the nearly 3 years of exceptional times after the 2020 Covid pandemic shocks, China’s economic surprise index has not been this low since 2015:

On China markets, investor allocation was active in July this year, with public fund AUM reaching new highs, up over 1 trillion CNY monthly, of which equity fund AUM rose 127.8 billion CNY from end June to 2.83 trillion CNY. Hybrid fund AUM slipped 41.43 billion to 4.59 trillion CNY. Bond fund AUM grew 178.69 billion to 4.94 trillion CNY. Additionally, influenced by overseas market gains, QDII fund AUM surged 42.498 billion in July to 401.302 billion CNY.

Fund Flows and Positioning

Last week markets were rangebound without clear divergence between defensive and cyclical stocks:

Growth underperformed value:

US equity mutual funds saw $4.3 billion of net outflows last week, the first outflows in 12 weeks:

But tech sector funds saw the largest inflows in 10 weeks:

Net leverage for US equity hedge funds reached 70% in Q2 but has since declined to 65% last week, below the 50th percentile of historical data over the past 5 years, indicating hedge fund positioning is not stretched currently with room to add:

US bond funds extended a record streak of inflows, for 28 straight weeks (+$5.2bn), the longest run since at least 2010:

Sentiment Indicators

Goldman Sach’s sentiment indicator for US stocks dropped from 0.8 previous week to 0.6 last week, still in neutral zone:

AAII bullish percentage declined sharply while bearish rose markedly, first time bearish exceeded bullish since early June, a healthy mean reversion after sentiment got overly optimistic:

CNN Fear & Greed index was basically flat last week after the prior week’s big drop:

Cryptocurrencies

IRS Discloses Stricter Tax Reporting Requirements

The US Treasury Department and Internal Revenue Service (IRS) have proposed new rules that plan to require crypto trading platforms (such as Coinbase and Kraken) to report detailed information on customer transactions like capital gains and losses from 2026 onwards — similar to existing requirements for stock and bond brokers. This measure aims to crack down on crypto tax evasion and increase transparency.

This news is clearly a notable negative for the crypto industry in the medium term as it will further reduce potential investment returns, but the market may not be sensitive to it yet given the long implementation timeline until January 2024. But in the long run it should be positive for the industry, as it will help bring more compliant use cases.

Stablecoin Flows

Per Glassnode’s metrics, centralized exchange stablecoin balances barely changed, with a minor $4.4 million outflow:

Total on-chain stablecoin supply increased substantially by $1.22 billion, the largest growth in ten months, but almost entirely attributable to DAI, with limited impact on market liquidity:

MakerDao’s treasury has locked up 1.26 billion DAI in the past month, corresponding to 24% of the total DAI supply, so DAI growth is almost entirely due to the treasury.

Spotlight on AI Leader NVDA’s Earnings

Nvidia’s data center revenue beat expectations substantially when reported last Wednesday:

- Nvidia reported Q2 revenue of $13.5 billion, above the company’s $11 billion guidance.

- Notably, data center revenue surged 171% yoy, with cloud service providers making up 50% of the mix versus 40% last quarter.

- Growth was strongest from US customers, while China contributed 20–25% of total revenue.

- Surging demand allowed Nvidia to charge higher prices for its chips. Gross margins hit 70.1% in Q2, up from 43.5% a year ago.

- For Q3, Nvidia guided to $16 billion in revenue, allaying some concerns about potential supply chain bottlenecks. Nvidia assured that its supply would increase each quarter over the next year, even in the face of potential US export restrictions.

The $25 billion stock buyback announcement also briefly excited markets, the 5th largest buyback announced by a US company this year. Despite the staggering amount, the repurchase represents just 2.1% of Nvidia’s nearly $1.2 trillion market cap, even below the S&P 500’s historical 2.58% buyback yield.

For reference, other major tech and growth companies have announced 2022 buybacks of: Apple $90 billion, Alphabet $70 billion, Meta $40 billion.

Nvidia CEO Jensen Huang said he expects $1 trillion will be spent globally over the next four years on AI data centers, including GPU upgrades. According to Huang, the bulk of the spending will come from cloud service providers and other major tech firms including Amazon, Microsoft, Google, Meta etc, who are aggressively pursuing generative AI.

Some analysis points out Huang’s pie may be too big, because the combined cash and cash equivalents of Amazon, Microsoft, Google and Meta currently total just $334 billion. Even factoring in new cash flows generated annually going forward, it falls far short of Nvidia’s $1 trillion 4-year estimate.

Nvidia stock rallied in the days leading up to the report, surging over 6% on Thursday to touch record highs intraday before paring gains at the close. It then plunged 2.4% the next trading session but still booked a 3.4% gain for the week.

Wall Street analysts collectively raised their price targets on Nvidia following the report. It currently has an average target of $640.71 per FactSet. The stock closed Friday at $460.18.

Notable investor Cathie Wood was unmoved by Nvidia’s blowout results. She sold millions worth of Nvidia stock over three days, insisting valuations reflected the opportunity and sticking to her strategy of selling into strength. She commented: “We think Nvidia’s in a great position to provide the picks and shovels for AI over the next five years. But that’s known, and it’s in the price.”

As we noted last week, markets had pinned high hopes on Nvidia’s earnings to buoy sentiment, but even with the big beat and strong guidance reported Wednesday, the lift ultimately did not sustain. Some analysis points out this is a signal of bullish momentum being “exhausted” this year, portending further declines ahead.

Michael Wilson, chief US equity strategist at Morgan Stanley, agrees with this take. He said despite Nvidia’s stellar results, the market decline on Thursday suggests the fuel for this year’s rally has been exhausted, presaging lower levels ahead. Thursday’s market reaction was a textbook top. Wilson explains, “The market tops on good news and bottoms on bad news. I can’t think of better news than Nvidia. Nvidia’s failure to lift markets is a negative technical sign upside momentum is exhausted. Now we need a new narrative to get the market excited again, but I’m not sure what that is.”

Bank of America strategist Michael Hartnett concurs with Wilson’s view. He believes that with rates higher for longer and the impact of Fed liquidity drain more pronounced, AI’s boost to stocks will fade in H2 2022, leading to tech stock pain.

Hartnett expects H2 2022 will be the period of trouble rather than the era of new AI. Because the correlation between Fed liquidity and tech stocks remains high, with the Nasdaq near historic highs while the Fed balance sheet is shrinking rapidly, which is incongruous.

Institutional Views

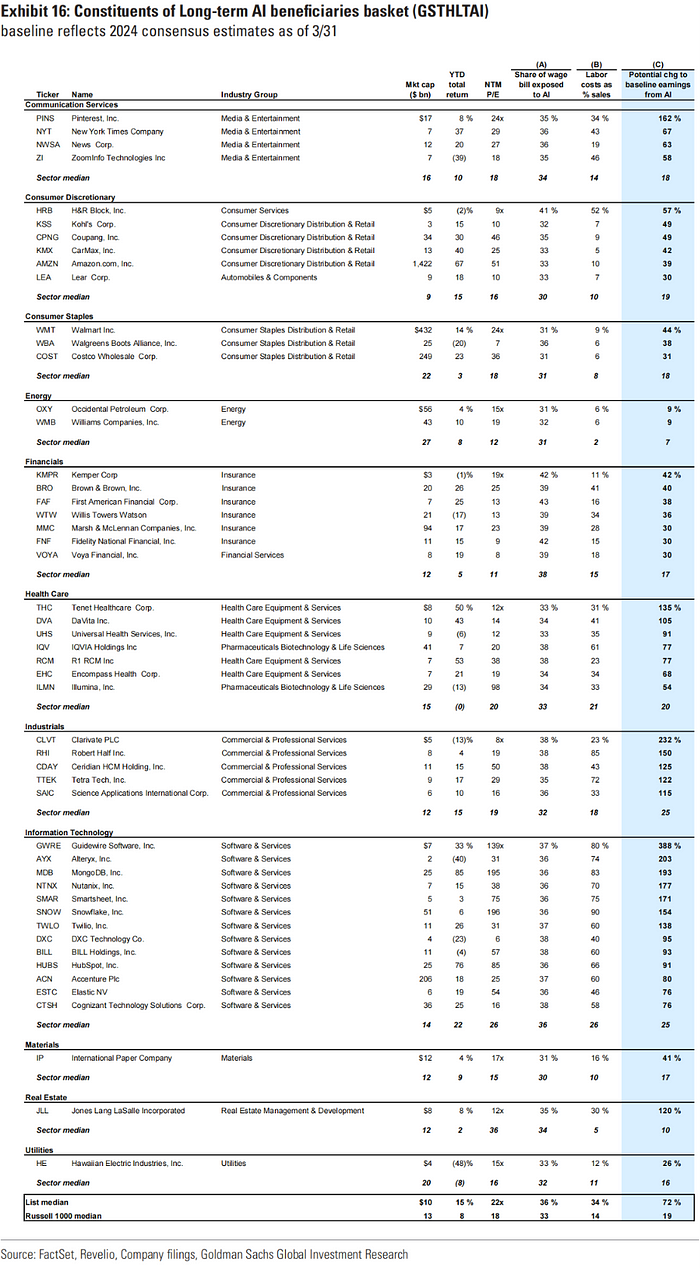

If short-term AI beneficiaries are already overvalued, then which long-term beneficiary stocks should be bought?

Goldman Sachs economists calculated the share of AI-automatable wage bills for 1,000 companies. They used US occupational task content data from over 900 occupations in the ONET database, estimating total automatable labor savings by occupation, assuming AI can perform tasks up to ONET “level” 4 difficulty.

They then took importance and complexity weighted averages of core work activities for each occupation, estimating the share of total labor that AI has potential to substitute, then calculated each company’s labor cost as a share of revenue based on global employee count and median salary from annual filings. Combining the two metrics gives potential earnings lift under constant profit margin and constant revenue assumptions.

Chart: Valuation logic

This gives two “treasure maps” for long-term AI beneficiaries, though as always we caution light conclusions and heavy logic for those interested to analyze or refining further:

The median EPS upside for this basket selected by Goldman is 72% above consensus by the time AI is widely adopted. Despite this, the basket has outperformed the S&P 500 by only 6% YTD, far less than short-term beneficiaries, indicating much of the potential productivity gains are not yet priced in. The profit margin expansion may not be permanent but investors could speculate on the possibility.

This Week’s Focus

US August jobs report, July PCE, progress on new fiscal year budget deal in Congress, US Treasury Secretary’s China visit, China/Europe/US PMIs, Eurozone August CPI.

September, upcoming next week, has historically flat performance for US stocks, averaging a 0.7% decline in September for the S&P 500 since 1945, the worst performing month of the year.