Duet Protocol Global Market Recap and Outlook — 20230821

Global major stock indices experienced three consecutive weeks of decline, with the S&P 500 and Nasdaq recording their most significant drops since the March banking crisis and late last year respectively, as concerns about higher bond yields and inflation are heating up, coupled with worries about a worse-than-expected slowdown in the Chinese economy and its debt crisis. Market sentiment, after being highly optimistic in July, now appears to have retraced back to the neutral zone, with data showing some institutional buying at the lows in recent weeks.

Stocks

The S&P 500 index fell more than 5% from late July, the Nasdaq 100 and Russell 2000 indices fell close to 7%, the CSI 300 index fell 5.7%, the Hang Seng Index fell nearly 11%, the Nikkei 225 fell 5.5%, and the Dow Jones Industrial Average fell relatively moderately. Nevertheless, given the gains of around 20% in the stock market since the beginning of the year, the pullback so far still remains within the healthy range and has not yet triggered a significant deterioration in market sentiment.

The divergence in declines is mainly due to the change in investment style, interest rate and inflation environment, and the composite reflection on earnings prospects.

The Dow Jones Industrial Average is mainly composed of large, stable, and long-established companies. In an environment of rising inflation and interest rates, investors may be more inclined to invest in these defensive companies. At the same time, the Nasdaq index is mainly composed of technology and growth stocks, while the Russell 2000 index is mainly composed of small-cap stocks, which may seem riskier in the current environment. Highly valued growth stocks (such as many Nasdaq constituents) may come under greater pressure as higher capital costs may erode future earnings prospects. In contrast, many of the Dow’s companies may perform better in an inflationary environment as they may more easily pass on rising costs to consumers.

By sector last week, biopharma, communication services, energy sectors performed well, while non-essential consumer sectors like autos, durables, transportation & leisure lagged.

With broad-based but differentiated declines, inter-stock (0.15–0.18) and inter-sector (0.33–0.35) correlations bounced back slightly:

Rates

Driven by supply pressures and strong economic data, the 10-year US Treasury yield hit its highest level since October last week at 4.33%. In contrast, 1–12 month yields barely changed. In the UK, with inflation metrics still robust and wage growth exceeding expectations, 10-year gilt yields jumped to 4.75% last Monday, the highest level since October 2008.

Concerns over China’s deteriorating real estate crisis and its impact on the country’s faltering economy have also exacerbated negative sentiment at times.

Chinese real estate giant Evergrande filed for bankruptcy in New York Thursday evening. The property distress has been a major drag on the troubled Chinese economy. Evergrande’s news came after another Chinese real estate giant, Country Garden, recently warned it could lose billions of dollars in the first half of this year. Moody’s downgraded the company, citing “increased liquidity and refinancing risks.”

Overall, the stock market pullback reflects more of a repricing of rate and inflation expectations rather than a signal of the economy completely losing momentum. Markets were overly optimistic in evaluating the outlook amid rising rates over the past few months, as measured by the Citi economic surprise indices, macro momentum still remains with economic surprises rebounding this summer in both the US and Europe:

Regarding the bond market, the rise in 10-year yields is not a signal that the Fed will hike further aggressively in the future. Mainly because the previous rise in long-term yields did not match the rise in short-term yields, the recent adjustment is not surprising, because either short-term yields will come down, or long-term yields will rise up, the bond market structure should not remain distorted for long, Fed rate hike expectations have come to an end, marginal changes have limited impact on the rate market. In addition, the sharp narrowing in long-short yield curve inversion since August can also be seen as a signal of long-term economic growth expectations rebounding:

Currencies

The US dollar followed yields higher, with DXY touching two-month highs last week. USD/JPY briefly rose to 146.2, the weakest level for the yen since November last year, beyond the area in September and October last year that prompted intervention by Japanese authorities. But Japanese Finance Minister Shunichi Suzuki said last week that authorities did not intervene based on absolute currency levels.

The Chinese yuan fell below 7.3 last week, hitting its lowest level since October last year, but rebounded sharply on Thursday and Friday due to the PBOC’s stance defending the yuan and a big lift in the fixing. USDCNY eventually held around 7.28.

Over the last three days of last week, the PBOC set the onshore dollar/yuan fixing at around 7.2, about 1,000 pips stronger than market prices. This represented the largest-scale defense of the yuan via the fix on record. The reference rate limits intraday moves in the spot rate to 2% on either side, with the PBOC theoretically committed to unlimited intervention to keep the yuan stable. In addition to lifting the fixing, state banks were said to have sold dollars and bought yuan directly in the spot market last week.

Earlier on Monday last week, the PBOC had just cut rates, with more monetary and fiscal stimulus measures expected soon, the widening rate differential could lead to continued depreciation pressure on the yuan. But currently, mainstream institutions do not expect significant further devaluation of the yuan from current levels.

For years, China has been highly sensitive to any wild swings in the yuan, as the speculative attacks that accompanied the 2015 yuan devaluation are still fresh in memory. The risk of a vicious cycle of rising pessimism, capital outflow from China, and potentially severe devaluation is present now. Hence the necessity of appropriate intervention.

Hot Topics

- *Federal Reserve Survey: U.S. Consumer Short-Term Inflation Expectations Hit a New Low Since 2021**

According to a survey released by the Federal Reserve Bank of New York on Monday, the short-term inflation expectations of U.S. consumers for the year in July dropped from 3.8% to 3.5%, the lowest since April 2021, marking the fourth consecutive month of decline. Inflation expectations for both three and five years also declined from 3% to 2.9%.

- *Bank of Japan: July Service Industry Inflation Reaches 2% for the First Time in 30 Years**

The CPI rose by 3.3%, in line with expectations. However, the “core-core CPI,” excluding energy and food, rose by 4.3%, the fastest since 1981.

- *Federal Reserve Minutes Lean Hawkish: Warning of Significant Inflation Upside Risks and Being Wary of Stock Market Rise**

The minutes indicate that most decision-makers still see significant upside risks to inflation, which may require further interest rate hikes. Many believe that even if rates are lowered, they may not stop the tapering process. Almost all decision-makers felt that a 25 basis point rate hike was appropriate in July, with two advocating for maintaining the current rate. Fed staff no longer expect a mild economic recession this year and project PCE inflation to drop to 2.2% by 2025.

U.S. Inflation Stickiness Reappears After Energy and Food, Used Car Prices Rise for the First Time in Four Months

Statistics for the first half of August show a month-on-month increase in wholesale used car data in the U.S. for the first time in four months. The market is concerned that, following the rebound in energy and food prices, this could be another sign of prolonged inflation.

*U.S. Retail Sales in July Increased by 0.7% Month-On-Month, Exceeding Expectations, Largest Increase Since January**

Reaching $696.4 billion, surpassing the previous 0.3% (revised to 0.2%) and market expectations of 0.4%, this was the largest increase in six months. Retail sales account for about one-third of all consumer spending and are often seen as a barometer of the U.S. economy. Bolstered by continued real wage growth, U.S. retail sales in July exceeded expectations, showing a robust economic performance.

- *China’s U.S. Treasury Holdings Drop to a 14-Year Low**

On Tuesday, August 15th, the U.S. Department of the Treasury released the Treasury International Capital (TIC) report, showing that as of June, China’s U.S. Treasury holdings had declined for the third consecutive month. The holdings decreased by $113 billion month-on-month, dropping to $835.4 billion, the lowest since June 2009.

However, China’s foreign exchange reserves rose to $3.193 trillion at the end of June, showing an overall upward trend for the year.

Google’s “Most Powerful Model” Gemini Shows Promise, Expected to Launch in the Fall**

Media reports suggest that Google’s new powerhouse, Gemini, combines the capabilities of GPT-4, Midjourney, and Stable Diffusion. It can also analyze charts, create graphics with text descriptions, and control software with text or voice commands.

- *Bridgewater’s Flagship Fund Turns Bearish on U.S. Stocks and Bonds in Late July**

Bridgewater informed investors that in late July, its flagship fund, Pure Alpha, was moderately bearish on U.S. stocks and bonds. Of the 28 assets analyzed by the fund, 15 were bearish, including the U.S. dollar, metals, and global stocks. The most bullish positions were in the Singapore dollar and the euro.

**Market Sentiment**

Earlier this year, there was a great deal of pessimism in the market. The shift from pessimism to optimism powered the stock market’s rebound. Now, we’re seeing a reversal of this overly optimistic sentiment.

The CNN Fear & Greed Index has significantly fallen to its end-of-March levels, currently reading 45, which is in the neutral range.

The AAII Investor Survey shows a significant drop in bullish sentiment from 44.7% to 35.9%, with bearish sentiment rebounding for two consecutive weeks, currently at 30.1%.

Goldman Sachs’ institutional position sentiment indicator has risen from the previous week (0.7–0.8).

Financial tension levels have sharply risen to their highest since March.

Bank of America’s survey shows that investor pessimism is at its lowest since February last year. Investors still expect global economic growth to soften over the next 12 months but believe central banks can achieve a soft landing during this period.

Current investor asset allocation is at its lowest equity underweight level in 16 months, with the largest overweight in tech stocks in over two and a half years.

The cash allocation ratio dropped from 5.3% in the previous month to 4.8%, the lowest since November 2021.

**Capital and Positions**

- *Overall Holdings**

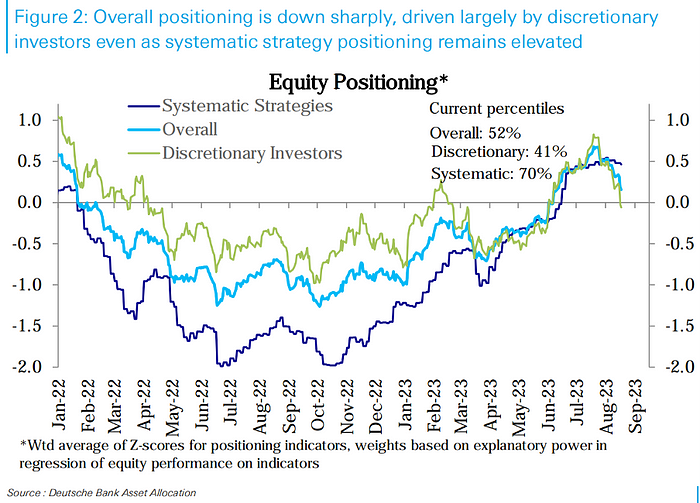

Deutsche Bank’s aggregated U.S. stock position levels have fallen for the fourth consecutive week to a two-month low (at the 52nd percentile historically). The decline is primarily driven by discretionary strategies, with their positions slipping just below neutral (at the 41st percentile). Systematic strategy funds remained largely unchanged over the past week, maintaining their highest levels since the end of 2021 (at the 70th percentile historically).

- *Sectoral Positions**

Holdings in Technology (73rd percentile), Staples (78th percentile), Discretionary (83rd percentile), and Communication Services (84th percentile) remain overweight but have decreased this week.

Industrials (72nd percentile) saw a decline but remain moderately overweight, as does Energy (70th percentile).

Real Estate (40th percentile) positions are moderately underweight and remained largely unchanged, while Financials (33rd percentile) are underweighted and have declined this week.

Healthcare (37th percentile) and Materials (33rd percentile) remain underweight and stable, whereas Utilities (17th percentile) are underweight and in a declining trend.

- *Fund Capital Flows**

Global equity funds saw a net outflow of $21 billion, primarily driven by a $52 billion outflow from the U.S. European markets experienced their 23rd consecutive week of net outflows (-$13 billion), while emerging markets saw a net inflow for the 6th consecutive week ($37 billion), primarily into Chinese funds, albeit at a slower pace than last week. Money market funds saw accelerated inflows, reaching $218 billion, marking the fifth consecutive week of inflows. The net inflow for bond funds significantly slowed down to a five-month low (+$0.3 billion).

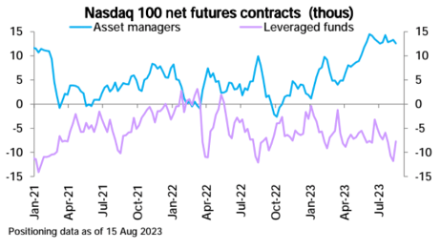

- *Futures Data:** Despite the pullback in the spot market, net long positions in U.S. stock futures increased for the third consecutive week as of last Tuesday. This is primarily due to an increase in net long positions in the S&P 500 and Nasdaq 100, with a decrease in net long positions for the Russell 2000, which is very close to neutral.

Of particular note, the increase in net long positions last week was mainly attributed to the more sensitive leveraged funds.

In other futures markets, bond net shorts declined for the 2nd straight week, mainly on reduced net shorts in 5-year and 30-year bonds, while 2-year and 10-year net shorts increased. In FX, dollar net shorts rose, primarily from increased euro and pound net longs, while Swiss franc and yen net shorts declined. Canadian dollar net shorts increased, and Aussie net shorts also rose. In commodities, oil net longs edged down slightly. Silver and gold net shorts increased, reducing gold net longs for the 4th consecutive week. Copper net shorts also increased.

Goldman PrimeBook Data

As the market declined, hedge funds shorted US ETFs last week at the fastest pace since September 2022, adding over 7% of the market cap in shorts in a single week. But this may not necessarily be a pessimistic signal, as they observed increased trading activity in US stocks over the past few sessions, with investment managers adding to equity exposures while also increasing beta hedges, while ETFs typically represent broad market or sector beta.

Crypto Stablecoin Flows

On-chain stablecoins saw net outflows for the 9th consecutive week, with a substantial $1.13 billion outflow last week, the largest single-week outflow since April 2 this year.

But exchange stablecoin balances rose for the first time in two weeks, increasing by $240 million net.

This Week’s Focus

The main catalysts driving markets this week are Powell’s speech at the Jackson Hole symposium on Friday, and Nvidia’s (NVDA) fiscal Q2 earnings on Wednesday.

Jackson Hole Symposium Preview

Taking place August 24–26. This year’s theme is “Structural Change in the Global Economy” with a particular focus on the resilience and potential inflationary risks in the global economy. Jackson Hole may be a decisive moment, with markets watching closely for any signal from the Fed on expectations for higher neutral rates, as that could be interpreted hawkishly by markets, implying higher rates to slow the economy.

Focus of Powell’s speech:

Powell is expected to lean heavily on recent data, including the latest CPI and Core PCE inflation reports.

He is expected to emphasize some progress made on combating inflation but will likely stick to his recent comments about the need to remain vigilant. He may be relatively upbeat on the state of the economy and will likely continue emphasizing completing its price stability job, including achieving below-trend growth.

UBS believes Powell may retain enough of a hawkish stance to leave the door open for more hikes but will stop short of putting a September increase on the table.

Bank of America said Powell will likely reiterate the Fed’s commitment to its 2% inflation target and push back against market pricing for the extent of hikes next year. The bank said that given the tremendous uncertainty around estimates of neutral rates, it does not expect any major pivot from the Fed on neutral rates at this meeting.

Nvidia (NVDA) Earnings Preview

Nvidia (NVDA) will report fiscal second-quarter results after the close on Wednesday in the US, which will be the biggest test yet of the AI hype cycle that has swept markets over the past 8 months. It will demonstrate whether the AI fever that has gripped markets over the past 8 months has actually translated into economic value. Because while Google and Microsoft delivered positive earnings growth last quarter, they did not attribute the growth to AI, crediting it to increased revenue from their existing businesses instead. Revenue at Microsoft’s AI-driven New Bing unit actually declined 4% last quarter.

Key metrics to watch for NVDA include:

Revenue: Analysts expect $11.1 billion vs $6.7 billion a year ago, implying 65% yoy sales growth.

Gross margins: Declined last year, rebounded to 66.8% in Q1.

Data center revenue: Has been growing steadily. Continued growth will quantify Nvidia’s momentum in AI.

Gaming revenue: Plunged in Q2 last year, downtrend expected through FY2023.

EPS: Q2 EPS expected at $2.07 vs $0.51 a year ago, up 305%.

Nvidia currently trades at a TTM P/E ratio of 146x, GAAP P/E of 222x, P/S ratio of 43x, and P/B ratio of 45x. This is an extremely steep valuation. Of course, Nvidia’s expected growth is also extremely high, and if the company hits expectations, growing revenues at a CAGR of several hundred percent over the next few years could quickly catch up to the extreme valuation.

Market Comments

[Wall Street warns 5% Treasury yields could become the new normal, with inflation potentially forcing the Fed to hike rates to 6%]

Bank of America warned investors to brace for the return of 5% Treasury yields, bringing the bond market back to pre-financial crisis levels. Given the 3.7% average inflation in personal consumption expenditures in Q2, the Fed may be forced to tighten policy benchmarks to at least 6%. Meanwhile, the yield curve inversion shows the risk of a US economic recession remains in the near term.

[JPMorgan warns a major tailwind for the US economy could be disappearing as consumers’ excess savings get depleted]

JPMorgan estimates that accumulated excess savings for US consumers peaked at $2.1 trillion in August 2021 and turned negative at -$91 billion in June 2022. Household liquidity surplus supported by cash and cash-like assets is currently around $1.4 trillion but will be depleted by May next year, and the liquidity may not necessarily support consumption above-trend levels.

The End.

Join us:

Github| Medium| Telegram| Twitter | Website |Discord | YouTube