Duet Protocol Global Market Recap and Outlook — 20230807

Overview

● Last week, influenced by the downgrade of U.S. Treasury bonds, long-term bond prices plunged and stock indices of major developed countries fell. Despite a slight rebound after the release of U.S. employment reports on Friday, all gains were eventually erased.

● Despite good overall performance of U.S. stock Q2 reports last week, there was no further rise in the overall stock market. Macro data remain robust but are already nearing their upper limits of expectations.

● Global risk appetite declined, with emerging market currencies generally falling sharply, the U.S. dollar strengthening, and gold prices being suppressed. However, oil prices rose due to news that Saudi Arabia will voluntarily cut production until September or even later.

● Cryptocurrencies were briefly boosted by the downgrade of U.S. Treasury bonds, but ultimately fell along with the global risk aversion. Stablecoins flowed out of both blockchain and exchanges.

● Given that U.S. stocks have not adjusted for more than four and a half months, a 3–5% minor correction would not be surprising, a period that has significantly exceeded the typical 2–3 month adjustment cycle.

Market Highlights

U.S. Treasury yield inversion narrows: Last week, the gap between the two-year and ten-year Treasury yields narrowed by 20 basis points, the largest contraction since the banking crisis in March 2008. This was mainly due to a faster rise in long-term interest rates, with the ten-year Treasury yield rising 8 basis points this week to 4.03%. After the release of July’s employment data, it once rose to 4.20% in early trading, only 2 basis points away from the peak on October 21 last year, which was the highest yield level since June 2008.

At the same time, the two-year Treasury yield fell 11 basis points to a nearly three-week low of 4.77%. The market’s expectation of a 25 basis point interest rate hike by the Fed at its September 20 meeting fell from 19% to 13%.

Bond yields rise in the long term and fall in the short term, accompanied by a decrease in interest rate expectations, a trend that has been rare in the past two years.

Emerging Markets: Last week, risk aversion emerged globally, putting pressure on emerging market currencies. For example, the South African Rand fell 4.5%, the Russian Ruble fell 3.9%, the Colombian Peso fell 3.7%, and the Renminbi fell slightly by 0.35%.

Stock Market Performance: The Nasdaq 100 index fell nearly 3%, the largest decline since the Silicon Valley banking crisis (March 10); the S&P 500 fell 2.3%, the largest single-week decline since March, and utility stocks fell sharply by 4.7%, the largest decline since September last year. The Dow Jones Industrial Average fell 1.1%. Major European stock indices also fell broadly, such as Germany’s DAX down 3.1% and France’s CAC 40 down 2.2%.

Apple plunges: Apple’s stock price plummeted 4.8% on Friday, bringing its weekly decline to 7.2% (the largest since November). Notably, Apple closed at a record high on Monday, with a cumulative increase of 51.6% since the beginning of the year.

Although Apple’s Q3 revenue and EPS exceeded expectations, service revenue reached a new high, and the revenue from the Greater China region was significantly positive, total revenue declined year-on-year for the third consecutive quarter since 2016, with all hardware product lines except Mac computers declining. Executives warned that Q4 revenue may continue to decline year-on-year, and iPad and Mac may experience double-digit percentage drops. After the news, Apple’s stock price briefly rose 1% before falling.

Apple’s P/E ratio is 30.59, compared to the S&P 500 index’s P/E ratio 25.56.

The impact of the U.S. Treasury downgrade: Fitch downgraded the U.S. credit rating, a decision widely criticized by Wall Street and Washington. There were hardly any views supporting their decision, with U.S. Treasury Secretary Yellen describing it as ‘flawed’ and ‘completely unfounded’, and former Treasury Secretary Summers calling the view that budget deficits and bipartisan disputes would lead to a U.S. Treasury default absurd.

In addition, Fitch also downgraded the long-term default ratings of U.S. mortgage finance giants Fannie Mae and Freddie Mac. The last time the U.S. rating was downgraded by the three major rating agencies was in August 2011 during the debt ceiling crisis when S&P downgraded the rating.

This event, coupled with the U.S. Treasury’s higher-than-expected bond supply, led to a rapid rise in long-term U.S. bond yields and a fall in global stocks. Bitcoin, riding the concept of a substitute for U.S. dollar assets, briefly rose above $30,000 after the event, but ultimately fell back as global risk aversion spread.

There is an interesting perspective that the downgrade in ratings reflects the current U.S. government’s long-term erroneous investments and expenditures. Unlike the past squandering of fiscal resources on effective investments such as highways, the current federal expenditures mostly flow into ineffective projects. The current government spending has promoted the military-medical complex and subsidized unproductive citizens, which is unsustainable. The U.S. must stop squandering resources to exchange for votes and fund ineffective projects, and should instead use them more to enhance future economic strength.

The situation in 2011 compared to today: Twelve years ago, when the U.S. lost its AAA rating from Standard & Poor’s (which it has yet to recover), S&P’s decision triggered a 4.8% drop in the S&P 500 on the day of the announcement on August 4 and a further 6.5% drop on August 8. In the subsequent two months, the stock market continued to fluctuate. Counterintuitively, however, investors flocked to government bonds and the dollar as safe-haven assets in an uncertain environment.

Compared with 2011, the stock market’s reaction to Fitch’s downgrade last week was more calm. Because before the game of the debt ceiling again in 2011 and S&P’s downgrade, investor sentiment was fragile, the memory of the global financial crisis was still fresh, economic growth was weak, and unemployment was as high as 9%. Now, economic growth in the past four quarters has been above trend, and the 3.5% unemployment rate is close to a historical low.

Undoubtedly, the continuous increase in federal debt, especially during periods of economic expansion, is worrisome, and it may be necessary to address this in the future through tax increases and spending cuts. However, U.S. bonds are still the safest assets globally. This has nothing to do with the credit rating of U.S. bonds, but is due to their large market liquidity and depth, enabling international investors to store funds and invest in government debt of the world’s largest economy. Its currency is also the global reserve currency. At present, no other asset class can become a practical substitute.

Therefore, I do not believe that the market will completely change its view on U.S. bonds. This is most likely an excuse for a stock market correction (the stock market has risen by 20%+ in the past two months), and at the same time, it provides a window for the extremely inverted yield curve to correct.

Debt and fiscal conditions deteriorate beyond expectations: To address the increasingly worsening fiscal deficit and continue to supplement the cash buffer, the U.S. Treasury Department has increased its net borrowing estimate for the current quarter to $1 trillion, significantly higher than the $733 billion predicted at the beginning of May. The continual deterioration of U.S. debt levels and fiscal deficit has triggered market concerns about a potential debt crisis in the future.

U.S. service sector activity cools: The U.S. ISM non-manufacturing index fell to 52.7 in July, with employment and business activity falling, but the price sub-index rose, with order backlogs expanding for the first time since February and healthy export growth. The Markit PMI data for the service sector, published earlier the same day, had a final PMI value of 52.3, a new low since February 2023, but the sixth consecutive month of expansion. The employment sub-index final value fell to 50.9, a new low since January 2023. However, it is worrying that service sector prices accelerated in July, which is usually associated with rising employee costs. This kind of wage-driven inflation persistence in the overall service sector naturally worries policymakers.

Money market fund records: U.S. money market fund assets increased by $29 billion this week, reaching a record $5.516 trillion.

Mortgage rates rise to an 8-month high: Freddie Mac’s 30-year fixed-rate mortgage rate rose 12 basis points this week, reaching an 8-month high of 6.92%.

Cooling in the labor market: In July, non-farm payrolls added 187,000 jobs, slightly lower than expected, and the lowest since December 2020. Most of the new jobs were in the healthcare and government sectors, while the more cyclical manufacturing industry contracted. Despite a cooling in labor demand in recent months, the unemployment rate dropped to a near-six-decade low of 3.5%. Wage growth exceeded expectations — average hourly earnings rose 0.4% in July, above expectations, a year-on-year increase of 4.4%. Increases of 0.4% in both June and July indicate a re-acceleration of wage growth. During the last bubble cycle, the year-on-year growth rate of average hourly earnings peaked at 3.5% in 2007 and 3.6% in 2008. The average growth rate during the 2009–2018 decade was 2.6%.

Additionally, the US job openings in June fell to a low since April 2021, at 9.582 million, indicating a slight softening in labor market conditions. Also, the quit rate declined to 2.4%, the lowest level since February 2021. A higher quit rate indicates a tighter labor market and confidence among workers in leaving their current jobs to seek better opportunities, and vice versa.

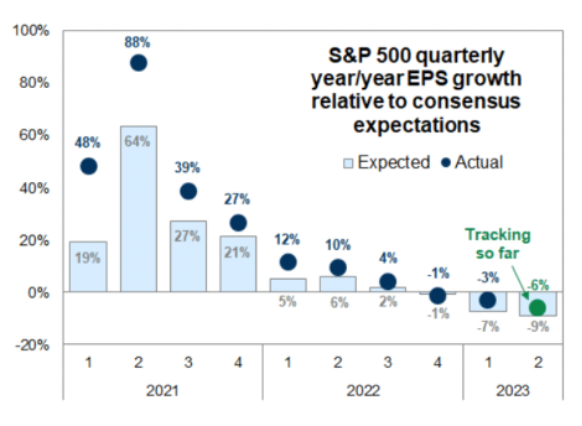

Q2 earnings report for US stocks -

Earnings beat expectations: As of last week, about 80% of S&P 500 companies exceeded consensus EPS estimates for the second quarter, indicating strong corporate earnings performance.

Revenue expectations missed: However, only 59% of companies beat revenue expectations, the lowest proportion in three years, reflecting potential revenue growth pressures in some industries.

Given the strong market performance over the past five months and the increasingly close linkage between stocks and bonds, the risk-return profile of US stocks under the current earnings backdrop isn’t very attractive.

China’s transaction activity in the US falls to a near-two-decade low:

This is a sign of geopolitical tensions between the two countries putting pressure on cross-border financial activity.

According to Dealogic data, US M&A investment from China so far this year is only $221 million, marking the slowest growth since 2006. The total amount for the same period last year was $3.4 billion. Aside from the US, Chinese transactions in Germany this year have only been $189 million, the lowest in over a decade, while activities in the UK and Australia have accumulated to $503 million and $228 million respectively.

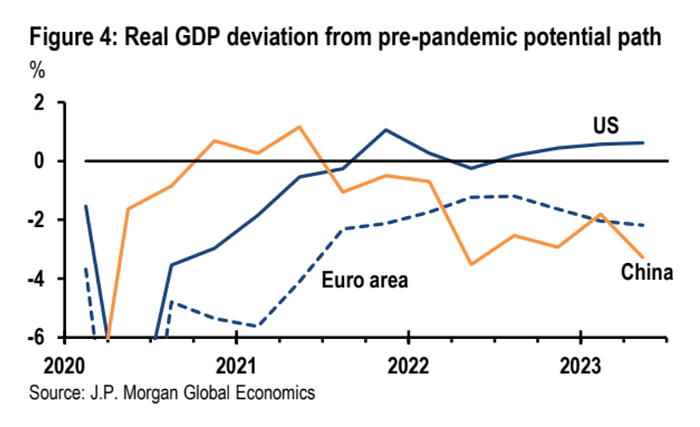

China’s output gap is promoting deflation (JP Morgan’s view):

China’s policy focus is shifting towards stabilizing the real estate market, promoting consumption, and restoring business confidence. Although policy changes may limit economic downside, it’s unlikely to close China’s significant output gap. Among major economies, China’s post-pandemic recovery is the weakest, with its GDP level still more than 3% below the pre-pandemic potential path:

Last week’s July PMI data (from the National Bureau of Statistics and Caixin) shows that industrial output grew modestly, non-tourism related services and construction growth slowed, indicating that this gap may widen further. The large gap between domestic demand and production capacity has lowered inflation, and it’s expected that this week’s July CPI will be negative (calculated on a monthly basis and year-on-year). Domestic concerns about deflation and growth will put pressure on the RMB. These dynamics have already pushed down export prices and should contribute negatively to global commodity prices in the coming period.

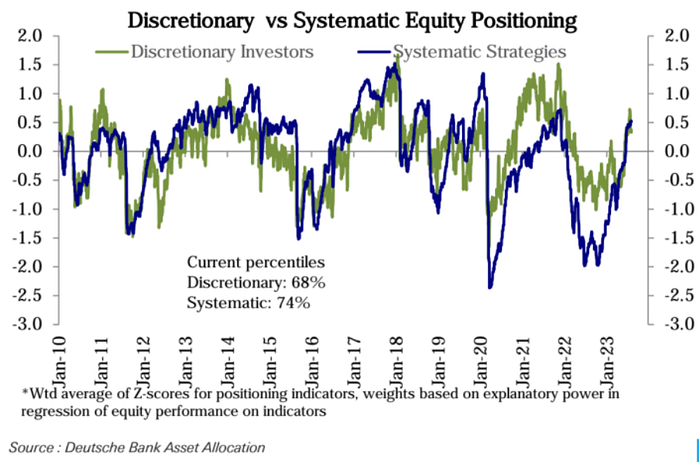

Position indicators:

Deutsche Bank’s overall stock market position metric fell slightly last week, with systematic strategy positions slightly lower (from 76 to 74 percentile), and discretionary investor positions declining for a second consecutive week (from 71 to 68 percentile), shedding about a third of the sharp increase since the end of May.

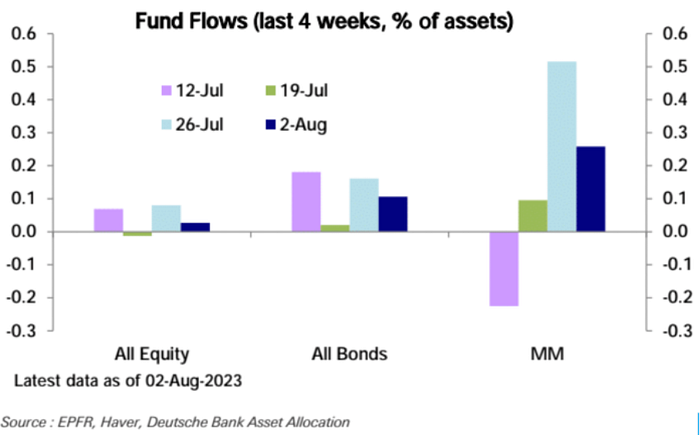

Last week, global stocks, bonds, and money market funds all recorded net inflows, although the inflows were lower than the previous week:

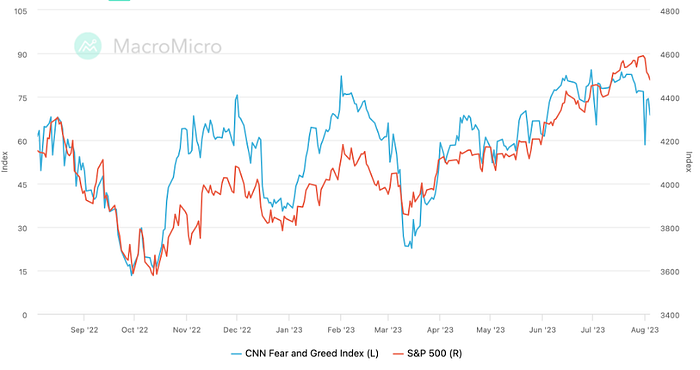

Investor sentiment indicators: Overheated investor sentiment cools down

At the end of the week before last, various signs indicated that investor sentiment was building up to near-feverish levels. The American Association of Individual Investors (AAII) sentiment index and the CNN Fear & Greed index both reached peaks of frenzy in 2021.

After several months of wild chasing, by the start of last week, investor positions had reached their highest levels of the year, and the market likely needed to digest this.

Last week, the CNN Fear & Greed index fell back slightly after a small rebound, currently reporting 69, below the “extreme greed” level of 75:

The AAII investor survey showed a slight rise in the bullish ratio last week, and the bearish ratio fell to its lowest since June 2021:

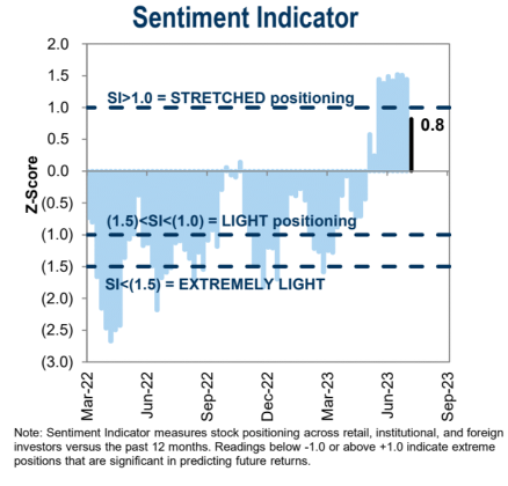

Goldman Sachs’ investor sentiment data fell sharply to its lowest level since June:

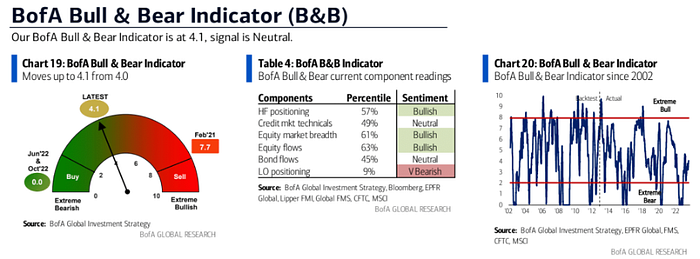

Bank of America’s Bull & Bear Indicator rose 0.1 to 4.1 last week, still remaining in the neutral range:

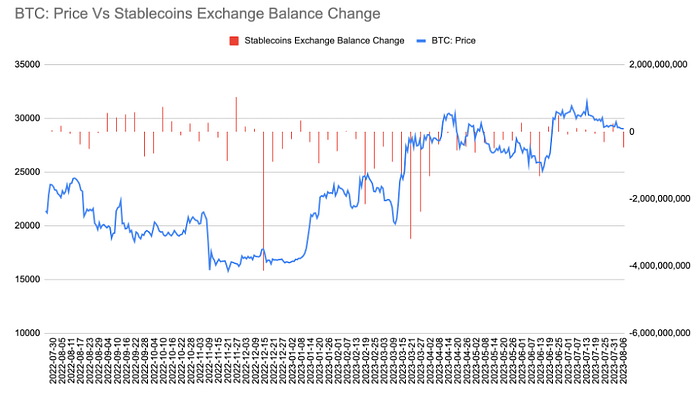

Cryptocurrency fluctuations

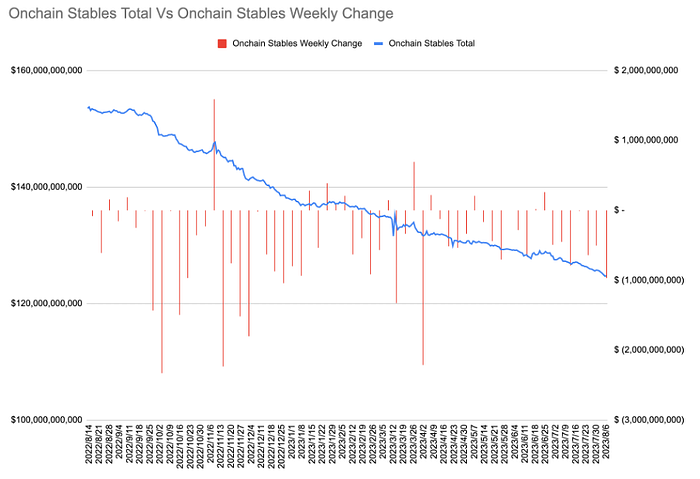

On-chain stablecoins have seen outflows for the seventh consecutive week, with a single-week outflow of $970 million, the largest single-week outflow in four months:

Last week, there was a net outflow of $476 million from exchange stablecoin balances to $18.06 billion, the largest single-week net outflow since June:

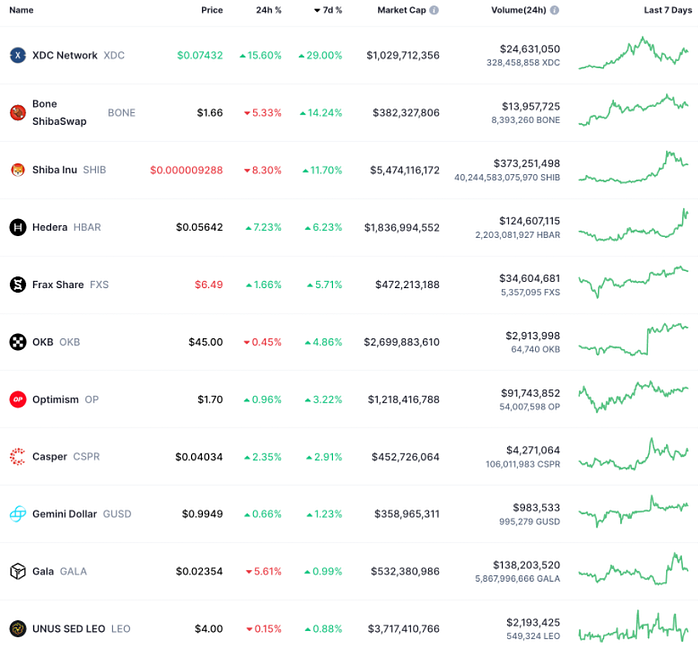

Weekly gains list for the top 100 cryptocurrencies by market cap:

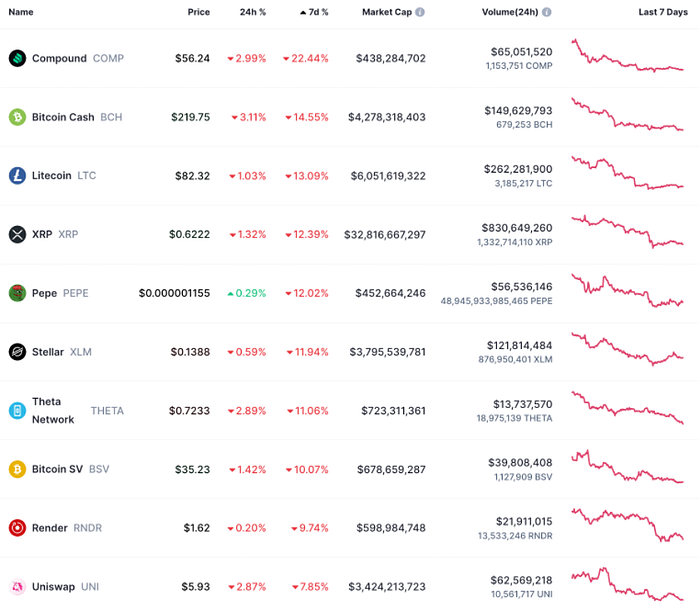

Weekly declines list for the top 100 cryptocurrencies by market cap:

Last week’s crypto news:

[Ethereum Futures ETF Application Wave]

In the past week, seven companies have submitted applications for Ethereum ETFs. ETFs tracking Ethereum futures are essentially investing in futures contracts for the second largest cryptocurrency in the industry.

[Hashkey Retail Trading Gets Permission]

The Hong Kong Securities and Futures Commission has approved HashKey Exchange’s upgrade to Licenses №1 and 7, allowing it to provide services to retail investors. To preheat the upcoming retail product, HashKey Exchange also recently launched a zero-fee spot trading promotion.

However, the platform currently offers a limited number of assets and trading pairs, officially supporting only BTC, ETH, USDT, SPiCE (the native token of the fully tokenized venture capital fund SPiCE) and 7 trading pairs, which cannot satisfy advanced crypto users.

Currently, HashKey Exchange does not support registration by users from jurisdictions where virtual assets are restricted, such as China, Japan, and the United States, and other sanctioned countries/regions.

[Curve Finance Founder Sells CRV to Raise $57.06 Million]

Since starting off-market sales on August 1, the founder of Curve has sold a total of 142.65 million CRV to 30 investors/institutions, raising $57.06 million in funds. Part of the proceeds were used to repay borrowings in protocols like FXS, mitigating market liquidation risks.

Buyers of Curve tokens include Sun Yuchen, Wintermute, DCF, DWF, Huang Licheng, Prisma Finance, Cream Finance and other individuals or institutions. Some analysts believe that the monopoly on CRV’s liquidity token has been broken, and Curve’s ecosystem may receive empowerment from related parties in the future, which is a medium and long-term positive for Curve.

Previously, Curve suffered a loss of over $60 million due to a flaw in the Vyper compiler for smart contract programming languages. Founder Michael Egorov borrowed $110 million in stablecoins by collateralizing CRV tokens on multiple lending protocols, and nearly faced liquidation under the influence of negative news. The market, including centralized exchanges, did not have such liquidity, and the matter temporarily came to a close with Michael selling the CRV tokens at a price of $0.4 (more than 20% below market price) to several well-known individuals in the industry through OTC.

For Curve’s products, the yield does not seem to be proportional to the risk. This event will also make people realize that even what looks like the safest DeFi project is not 100% safe. Without staking CRV tokens, the total APY for liquidity providers is only 1.5%. Even if you stake as many CRV tokens as possible or use yield aggregators like Convex, the APY you can earn does not exceed 3%.

[YGG whales begin to reduce holdings after a 200%+ increase]

Over the past week, the price of YGG tokens has risen by about 232%, and the market cap has reached about $150 million. Yesterday, two investors deposited a total of 3.57 million YGG (about $2.06 million) into Binance after the sharp rise. Among them, BITKRAFT Ventures deposited 1.57 million YGG (about $907,000) into Binance through Wintermute Trading and FalconX; an address starting with 0x639B deposited 2 million YGG (about $1.16 million) into Binance and currently still holds 2 million YGG (about $1.16 million).

[ARK Invest has reduced more than $18 million in Coinbase stocks this month]

As of last week, ARK Invest has sold a total of 208,859 shares of Coinbase stock in August, worth about $18.24 million.

Tokens unlocking this week:

Aptos (APT) will unlock approximately 4.54 million tokens at 8am on August 12, worth approximately $30.44 million.

ImmutableX (IMX) will unlock approximately 18.08 million tokens at 6am on August 12, worth approximately $13.31 million.

This week’s outlook

Economic data

● China’s July trade data is expected to remain weak, with year-on-year declines in exports and imports expected to continue

June trade data showed a continued slowdown in China’s foreign trade. Exports and imports both fell significantly below expectations, recording the largest monthly decline since 2020. The market expects the decline in exports and imports to continue in July, by 12.5% and 5.5% respectively, further highlighting the serious challenges facing the Chinese economy. The recurrent pandemic and worsening external environment are severely constraining China’s foreign trade.

● July CPI is expected to turn negative, and PPI may continue to decline

After June CPI and PPI fell to 0% and -5.4% respectively, China’s inflation data is expected to remain weak in July. Contraction in manufacturing activity and a slump in the real estate market have led to rising deflation expectations. Analysts predict that July CPI may slide further and turn negative, and the PPI decline may continue to widen, which will increase downward economic pressure. Stabilizing growth is the current policy focus.

● U.S. July CPI data may be more worrisome than expected

June U.S. CPI fell significantly, but the June CPI was the most “friendly” of the cycle so far. With the rebound in oil prices and the weakening of base effects, further significant falls in CPI will be difficult: analysts expect July CPI to rise 3.3% year on year and 0.3% month on month, higher than the 3% year-on-year increase and 0.2% month-on-month increase in June. Core CPI is expected to rise 4.8% year on year and 0.2% month on month, both the same as in June.

CPI and PPI data will have a key impact on Fed decision-making.

It should be noted that gasoline prices soared in July, up 6.84% year-on-year, the largest increase so far this year. Although the impact on the July report is limited, considering that gasoline has a weight of 3.4% in the CPI, inflation in August and September will be more severe. August inflation expectations have risen to 3.6%, and September expectations are at 3.37%, both revised up from previous expectations. Crude oil prices also surged nearly 16% in July, the largest monthly increase since 2022, and rising oil prices will undoubtedly push up future inflation.

Core inflation remains a focal point. Although the growth rate of the service industry and rents has cooled recently, it is still insufficient to bring down core inflation.

If inflation intensifies, long-term yield rates may be further adjusted upwards, implying that the valuation of risk assets may be under pressure.

Bond Auction

Last week, the US Treasury Department increased the quarterly issuance size of long-term bonds for the first time in over two and a half years. The increased borrowing needs of the US government also contributed to Fitch’s downgrade of the US AAA sovereign credit rating.

The Treasury Department said it would issue $103 billion in longer-term bonds during this week’s quarterly refinancing operations, comprising 3-year, 10-year, and 30-year bonds. This is higher than the previous total issuance of $96 billion and slightly higher than most traders’ expectations. It’s important to closely watch the auction’s bid interest rates and bid multiples, as the bond market sentiment is currently fragile.

Additionally, the Treasury Department expects the net issuance of securities in the third quarter to reach a record high of $1.007 trillion for the same period in history, up by $274 billion from the estimate in early May.

J.P. Morgan strategist Nikolaos Panigirtzoglou believes that even with the rebuilding of the TGA and the additional issuance of bonds causing a contraction of at least 4% in US broad liquidity. The bank defines “broad liquidity” as the sum of the money supply (M2) and institutional money market fund assets.

Key Earnings Reports

On Wednesday, August 9, Walt Disney and Roblox will release their quarterly earnings reports. As significant companies in the entertainment industry and the metaverse domain, their financial reports will attract high market attention. The growth of Disney’s subscribers and Roblox’s user data will be key indicators.

On Thursday, August 10, Alibaba will release its earnings report. As a leader in Chinese e-commerce and cloud computing, its financial report will directly affect judgments about the Chinese economy. Cloud computing and business growth will be the key points.

Thank you for reading Duet Protocol’s global market recap and outlook. Welcome to try Duet Pro, the RWA (Real World Asset) perpetual future trading platform with 100x leverage, and profit!

Join us:

Facebook| Github| Medium| Telegram| Twitter | Website |Discord | YouTube